This topic contains 15 replies, has 10 voices, and was last updated by ![]() Y_ 2 years, 8 months ago.

Y_ 2 years, 8 months ago.

- AuthorPosts

Canada’s House Price Bubble

Thanks to Wolf Richter of Wolfstreet and Tyler Durden of ZeroHedge for the material which has been edited for posting. The original articles are in the citation list.

During the first two weeks in May 2017, according to preliminary data from the Toronto Real Estate Board, home listings surged 47% from the same period last year even as sales plunged 16%. The average selling price dropped 3.3% from April – and this, after a 33% year-over-year spike in home prices in March and a 25% surge in April. Something is happening to Toronto’s blistering house price bubble.

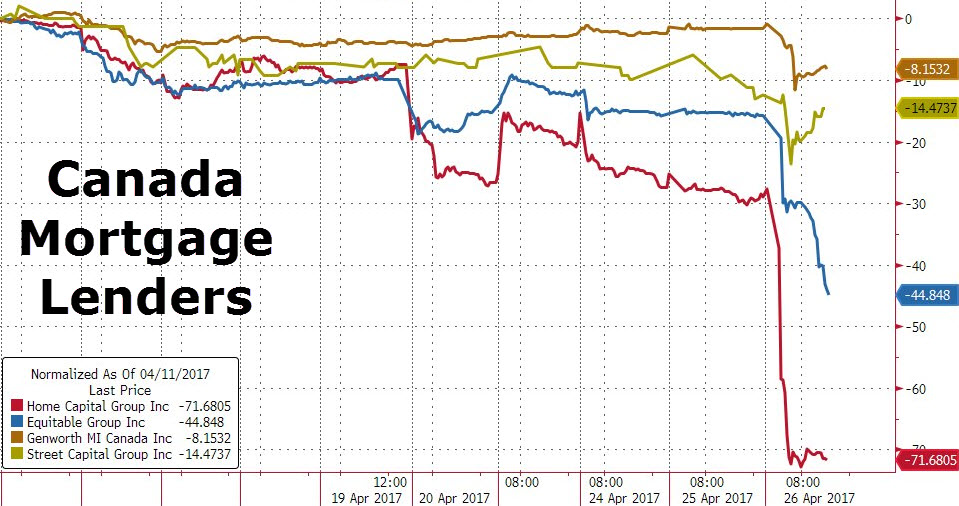

The ContagionCanada’s largest alternative mortgage lender, Home Capital Group, which focuses on new immigrants and subprime borrowers turned down by the banks, is melting down after a run on its deposits that crushed its funding sources. The industry is worried about contagion.

Home Capital Group, Canada’s biggest “alternative” mortgage lender, is not a bank – which today is part of its problem because it cannot create money to lend out; it has to obtain it first by attracting deposits and borrowing money through other channels.

Through its subsidiary, Home Trust, it specializes in high-profit mortgages to risky borrowers, with dented credit or unreliable incomes who don’t qualify for mortgage insurance and were turned down by the banks. This includes subprime borrowers

Since revelations of liar loans (what!, liar loans in Canada?!) surfaced in 2015, things have gone to heck. Now it’s experiencing a run on its deposits. Teetering at the abyss, it obtained a $2 billion bailout loan recently. The terms are onerous. And the next day to that loan the crux of the deal emerged – the amount of mortgages it has to post as collateral. It’s a doozie.

It sheds some light on what insiders think mortgages and the homes that back them are worth when push comes to shove. A bone-chilling wake-up call for the Canadian housing and mortgage market.

This is when the whole construct started falling apart:On July 30, 2015, it disclosed, upon the urging of the Ontario Securities Commission, the results of an investigation that had been going on secretly since September 2014 into “falsification of income information.” Liar loans.

It suspended 45 mortgage brokers who’d together originated in 2014 nearly C$1 billion in residential mortgages, or 12.5% of its total

On April 26, 2017, Home Capital announced that it was experiencing a run on its deposits. As of the end of March, its subsidiary Home Trust sat on about C$2 billion in high-interest savings accounts (HISA) it is offering to regular savers. But these folks were pulling their money out, it said, and the pace of the run was accelerating.

It also disclosed that it was finalizing a $2 billion bailout loan from the Healthcare of Ontario Pension Plan (HOOPP) which has about $70 billion in assets. The loan would “have a material impact on earnings….” So an expensive loan.

The Big Picture

At the same time, the provincial government of Ontario announced a slew of drastic measures, including a 15% tax on purchases by non-resident foreign investors to tamp down on the housing market insanity that left many locals unable to buy even a modest home.

It comes after Bank of Canada Governor Stephen Poloz warned in April that home prices are in “an unsustainable zone,” that the market “has divorced itself from any fundamentals that we can identify,” that there was “no fundamental story that we could tell to justify that kind of inflation rate in housing prices,” and that “It’s time we remind folks that prices of houses can go down as well as up. People need to ask themselves very carefully, ‘Why am I buying this house?”’

In May 2017 Moody’s Investors Service downgraded Canada’s six largest banks on concerns over their exposure to the housing bubble and household indebtedness that ranks among the highest in the world:

“We are seeing people who paid those crazy prices over the last few months walking away from their deposits,” Carissa Turnbull, a Royal LePage broker in the Toronto suburb of Oakville, told Bloomberg. She said they didn’t get a single visitor to an open house over the weekend. “They don’t want to close anymore.”

“Definitely a perception change occurred from Home Capital,” Shubha Dasgupta, owner of Toronto-based mortgage brokerage Capital Lending Centre, told Bloomberg.

“In less than one week we went from having 40 or 50 people coming to an open house to now, when you are lucky to get five people,” Case Feenstra, an agent at Royal LePage Real Estate Services Loretta Phinney in Mississauga, Ontario, told Bloomberg. “Everyone went into hibernation.”

“I’ve had situations where buyers are trying to find another buyer to take over their deal,” Toronto real estate lawyer Mark Weisleder told Bloomberg. Some clients want out of transactions, he said. “They are nervous whether they bought right at the top and prices may come down.” Home Capital had “a bigger impact on the market” than Ontario’s announcement of the new rules, he said.

“Home Capital is affecting things because people who can’t get mortgages from the banks rely on them and other b-lenders,” Lorand Sebestyen, an agent with iPro Realty in Toronto, told Bloomberg. “If you can’t get the mortgage then you obviously can’t buy anything and it’s going to affect the market, especially for the higher-priced properties.”

“It’s fear,” said Joanne Evans, owner of Century 21 Millennium, about the impact of Home Capital on housing. “It’s another contributing factor to the fear of ‘what’s going to happen?”

And it’s ever so slowly sinking in more broadly.

In Canada, the theory has spread that real estate values can never-ever go down in any significant way – on the theory that they always go up – because they didn’t take a big hit during the Financial Crisis, and because the prior declines have been forgotten. So optimism about rising home prices had been huge.

Now weekly polling data by Nanos Research for Bloomberg is showing the first signs of second thoughts. Two weeks ago, the share of people saying home prices would rise in the next six months was a record 50.1%. The following week, it dropped to 47.7%. In the most recent poll, it dropped to 46%.

But those who are able to sell at what appears to be the very tippy-top of the market are not complaining. Bloomberg cites business school professor Michael Hartmann who put his north Toronto home up for sale on May 17 sold it on May 22 for C$1.65 million, C$10,000 above asking price. He and his wife are planning to rent and see.

So, can a US-style banking crisis hit Canada?

This comes up constantly in discussions on the current house price bubbles in some cities in the US and Canada, and whether a US-style crisis could happen in Canada: The housing bust in the US during the Financial Crisis was marked by banks receiving “jingle mail” from homeowners who saw the value of their homes plunge and their equity turn negative. These folks just turned in the keys to the bank.

These “strategic defaults,” it is said, won’t happen in Canada because mortgages are “recourse,” and in the US they’re “non-recourse.” We hear this constantly. But it’s wrong.

In its working paper, the Richmond Fed tried to determine if there were differences in default rates in recourse states v. non-recourse states – “the first study looking at difference in how borrowers default,” it said.

In recourse states, banks’ collecting on residential “purchase” mortgages after default is limited to the value of the collateral (the home). If the debt is larger than the value of the home, usually determined by proceeds from the foreclosure sale, the lender is generally barred from trying to collect the remainder of the debt from the borrower.

In non-recourse states, lenders may obtain a “deficiency judgment” and try to recoup the mortgage debt beyond the value of the collateral.

For homes priced at origination substantially above the median price, “strategic defaults” were more likely in non-recourse states than in recourse states.

Some states require judicial foreclosures (in court), others require non-judicial foreclosures, and in some, both are an option. And there are numerous other laws that impact results.

In Canada, only Alberta and Saskatchewan are non-recourse provinces and only if it is not insured by the government’s mortgage insurer CMHC.

In the rest of Canada, mortgages are generally recourse loans. If the mortgage is insured, the CMHC may pursue the borrower for the deficiency.

But here’s the thing: In the US, only 11 states are non-recourse. Yet the housing bust and foreclosure crisis was spread across much of the country and crushed lenders in recourse states just as hard, including in Florida and Nevada.

It caused the government and the Fed to bail out the banks and the federal mortgage insurers (Fannie Mae and Freddie Mac).

In that respect, the US and Canada are on the same level: In a smaller part of the country, mortgages are non-recourse; in the vast majority of the country, mortgages are recourse. Government entities insure certain types of mortgages in both countries.

Mortgage-backed securities exist in both countries, as do subprime borrowers. Loans for down payments are a thriving industry in Canada that even the provincial government of British Columbia has now entered.

Recourse was no protection in the US against defaults and a financial crisis.

This shows that when housing implodes hard enough after an enormous bubble, and if the bust is associated with a broader economic downturn, as housing busts inevitably are, in the end, what happened in the US can happen in Canada.

The question now being asked, years too late:

How will this end?

Citations

http://www.zerohedge.com/news/2017-05-26/all-hell-breaks-loose-torontos-house-price-bubble

http://wolfstreet.com/2017/04/29/canada-house-price-bubble-what-are-homes-really-worth/

http://wolfstreet.com/2017/04/25/mortgages-u-s-canada-recourse-states-non-recourse-states/

Anonymous43one of my relatives bought a house just before the

florida housing bubble burst…paid $420K for a $200K house. Soooo taxes are assessed a year behind…not only upside down, but over paid in taxes the first year in. By buying this new place, they lost their homestead exemption status, so taxes went down the second year, then went up the third year about 20%.Homestead exemption, limits tax increases to 3%? houses bought before a certain date or 10 years of ownership, I forget.

buying the new house was a disaster…woman wanted a bigger better newer house, man wanted to stay put.

Yep, divorced a couple years later. predictable.

Very interesting. I had no idea Canada was on the verge of blowing apart their mortgage market. I wonder when that’ll hit the states again. It’s insane where I live, and exacerbated by the fact any actual home (not apartment, townhome, or condo) starts at $300,000.

one of my relatives bought a house just before the

florida housing bubble burst…paid $420K for a $200K house. Soooo taxes are assessed a year behind…not only upside down, but over paid in taxes the first year in. By buying this new place, they lost their homestead exemption status, so taxes went down the second year, then went up the third year about 20%.Homestead exemption, limits tax increases to 3%? houses bought before a certain date or 10 years of ownership, I forget.

buying the new house was a disaster…woman wanted a bigger better newer house, man wanted to stay put.

Yep, divorced a couple years later. predictable.

Thank you and this is THE lesson – you have hit the nail square on the head.

I believe – just as you describe here – most all these houses are bought BY men FOR females. And the man loses one way or the other.

Bubble… Meet Pin…

It is by caffeine alone I set my mind in motion, it is by the beans of Java that thoughts acquire speed, the hands acquire shaking, the shaking becomes a warning; it is by caffeine alone I set my mind in motion.

I wonder when that’ll hit the states again

In the US – for those men that can afford a house – there was the Glass-Steagall Act of 1933 (that was struck down by Clinton in 1999 and caused the housing bubble of 2008 by Freddie Mac) and now the Frank-Dodd Act in 2010 (which Trump wants to repeal).

The Volcker Rule of this Act puts a much-needed barrier between housing mortgage lenders and investment banks to stabilise the housing market to ensure sufficient liquidity in the system in case of mortgage defaults.

Effectively separating the investment and commercial functions of a bank, the Volcker Rule strongly curtails an institution’s ability to employ risk-on trading techniques and strategies when also servicing clients as a depository.

Dodd-Frank Financial Regulatory Reform Bill http://www.investopedia.com/terms/d/dodd-frank-financial-regulatory-reform-bill.asp#ixzz4iFnr7PnO

Once this Act is repealed all bets are off.

With a massive recession on the horizon, something has to give on the housing market in the west as a whole.

It’s going to be painful but it needs to crash and reset, housing especially is way out of reach for many working people which is ridiculous!

When housing was at a price where it should be many years ago, it was the utlimate vehicle for people to get ahead and have a comfortable retirement.

Now everything is beyond reach of the working folk. Again, it’s not gonna be pretty but things need to change!.

It’s going to be painful but it needs to crash and reset

Exactly….a cool down is not gonna cut it…there needs to be a solid CRASH.

Otherwise the middle class and the poor class will merge.

Even an engineer, here in Australia, cannot afford to buy a house on a $100K salary!

A tranquil mind is neither happy nor sad, it is uninfluenced by external conditions.

Thanks again man. Timely advice as I am currently talking with a good friend about his buying an apartment building and my own wishes to acquire one too. I am waiting still to observe what happens in the next year or two. His age group and deal make it a better time for him, but the price is 40k too high compared against the earnings potential. I advised him to wait as well and keep saving his nut of cash.

Thanks again man. Timely advice as I am currently talking with a good friend about his buying an apartment building and my own wishes to acquire one too. I am waiting still to observe what happens in the next year or two. His age group and deal make it a better time for him, but the price is 40k too high compared against the earnings potential. I advised him to wait as well and keep saving his nut of cash.

My pleasure bro – anytime. Hope this helps in some way.

Even an engineer, here in Australia, cannot afford to buy a house on a $100K salary!

I am in Sydney and as you say – general engineer salaries to houseprices are impossible and much more so for other types of employment

I mean you are paying about 40% – 45% tax off the top to begin with. Plus inflation. Your salary is about halved. Then you have super.

A house median of $1 150 000 here. Interest rate of 3.4% variable. That’s $40 000 a year on interest alone. for the first year. You could not buy a house here on your salary if you have no savings to offset the principal.

2008 all over again.

Love is just alimony waiting to happen. Visit mgtow.com.

The bubble will certainly pop soon.

I’ve been following the Baby Boomers as the key indicator here in Canada. The oldest are hitting 71 years of age now.

They were all buying in the 80’s. A time that saw record mortgage interest rates as currency was getting expensive with all the baby boomers buying.A good book on the boomers and their impact on housing prices in Canada is “When the bubble bursts” Hilliard Macbeth –

Up until recently we were probably seeing a couple of dynamics at play. People rushing into the market afraid that its now or never to buy a house. And retired people cashing out a little early trying to cash in on the bubble before it pops.

It appears that this door may be closing. Never the less older baby boomers may still want to sell as they age.As they sell the supply will increase. Combine this with the people who were panicked into buying in a now or never phase, realizing they are up to 1 million in debt and are now enslaved for the next 30 years.

Keep in mind that in Canada you can’t walk away from you house and mortgage. The debt follows you.

Factor in the extremely easy method to leverage you home equity and many Canadians are even further in debt.What can potentially follow doesn’t look pretty.

Anonymous14I saw two families fall apart in the SAME HOUSE across the street from me in 2008. First one the wifey was throwing pots and pans at the husband, she up and left with the kids, he had no job, was in construction and had been laid off for awhile. He ended up selling much of the inside of the house before he left (including the kitchen sink). I knew this because the next family that moved in the husband told me so. Well… He was also in construction and had no work for a couple of years… Wifey left him for another dude, but only after she got her fat ass in shape and found a good job, but after that, she was GONE…Classic stay with the provider as long as he was providing, then when he wasn’t PULL THE RIPCORD! I saw this all happen over a few months. I was like “why is she going walking/running all the time all of the sudden?”…

The system f~~~s men at every turn. Every single f~~~ing turn.

FIAT money is nothing more than a form of enslavement. Make it out of thin air, then enslave those you lend it to. Oh, and wage wars with it, endlessly apparently. The longer the cycle, the less buying power the people have due to inflation and wages not keeping up.

#493952

Reply |FIAT money is nothing more than a form of enslavement. Make it out of thin air, then enslave those you lend it to. Oh, and wage wars with it, endlessly apparently. The longer the cycle, the less buying power the people have due to inflation and wages not keeping up.

House always wins. Pun intended.

- AuthorPosts

You must be logged in to reply to this topic.

921526

921524

919244

916783

915526

915524

915354

915129

914037

909862

908811

908810

908500

908465

908464

908300

907963

907895

907477

902002

901301

901106

901105

901104

901024

901017

900393

900392

900391

900390

899038

898980

896844

896798

896797

895983

895850

895848

893740

893036

891671

891670

891336

891017

890865

889894

889741

889058

888157

887960

887768

886321

886306

885519

884948

883951

881340

881339

880491

878671

878351

877678